You found a house in rural Japan listed for ¥1,000,000 — roughly $6,500. You start imagining weekend renovations, tatami rooms, a garden with persimmon trees. But between the listing price and actually holding the keys, there is fees, taxes, and costs that can easily add 20-40% to your total outlay. Some arrive months after you thought the deal was done. This guide breaks down every single cost so you can budget with your eyes open.

Why the Purchase Price Is Just the Beginning

In most countries, the sticker price of a property is the main event. In Japan, it is more like the opening act. The Japanese real estate transaction system involves a distinct set of government taxes, professional fees, and registration costs that are largely unavoidable. Unlike some markets where closing costs are negotiable or bundled into financing, Japanese transaction costs are codified in law with specific calculation methods.

The gap between the listing price and total cost is proportionally larger for cheap properties. On a ¥50,000,000 house, transaction costs might add 6-8%. On a ¥1,000,000 akiya, they can add 30-50%. This is the key thing to understand about budget akiya purchases: the cheaper the property, the higher the percentage overhead.

Here is every cost you will encounter, in roughly the order they appear.

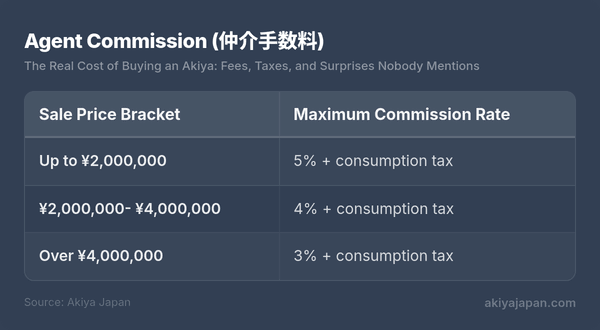

Agent Commission (仲介手数料 (chūkai tesūryō))

Japanese real estate agent commissions are not market-rate — they are legally capped by the Building Lots and Buildings Transaction Business Act. The maximum an agent can charge is set by a sliding scale based on the sale price:

For properties over ¥4,000,000, the simplified formula works out to:

(Sale price × 3% + ¥60,000) × 1.10 (the 1.10 accounts for 10% consumption tax)

So on a ¥10,000,000 property, the maximum commission is (300,000 + 60,000) × 1.10 = ¥396,000.

The Low-Price Property Exception

For cheap akiya, there is a special provision, originally introduced in 2018 and expanded in July 2024. When the sale price is ¥8,000,000 or below (doubled from the original ¥4,000,000 threshold), the agent can charge a flat maximum of ¥198,000 + consumption tax = approximately ¥330,000 (including tax) to cover the disproportionate work involved in low-value transactions. This is sometimes called the "low-price property mediation fee special rule" (低廉な空家等の媒介特例 (teirenka akiya-tō no baikai tokurei)).

This means a ¥500,000 property and an ¥8,000,000 property can have the same agent fee. On the ¥500,000 house, that ¥330,000 commission is 66% of the purchase price. Budget accordingly.

Note: Not all agents charge the maximum. Some charge less, especially if they are representing both buyer and seller (double-ending the deal). But most do charge the cap, and you should budget for it.

Registration and Licence Tax (登録免許税 (tōroku menkyo-zei))

When you buy property in Japan, the ownership transfer must be registered with the Legal Affairs Bureau (法務局 (hōmu kyoku)). This registration incurs two distinct taxes:

Ownership Transfer Registration Tax

This is calculated on the assessed value (固定資産評価額 (hyōka-gaku)) of the property — not the purchase price. This is a crucial distinction that trips up many buyers. The assessed value is set by the local government for tax purposes and is typically 50-70% of the actual market value for land, and often much lower for buildings (especially old ones).

- Land: 1.5% of assessed value (reduced rate, normally 2%, currently extended through 2026)

- Buildings: 2.0% of assessed value (standard rate; 0.3% if it qualifies as your primary residence and meets certain conditions)

Example: You buy a property for ¥5,000,000. The land's assessed value is ¥2,000,000 and the building's assessed value is ¥800,000. Your registration tax would be:

- Land: ¥2,000,000 × 1.5% = ¥30,000

- Building: ¥800,000 × 2.0% = ¥16,000

- Total: ¥46,000

On older akiya where the building has been heavily depreciated, the building's assessed value might be close to zero, which actually works in your favor here.

Mortgage Registration Tax

If you are financing with a mortgage (unusual for foreign buyers, but possible), there is an additional registration tax of 0.4% of the loan amount (0.1% reduced rate for primary residences meeting conditions).

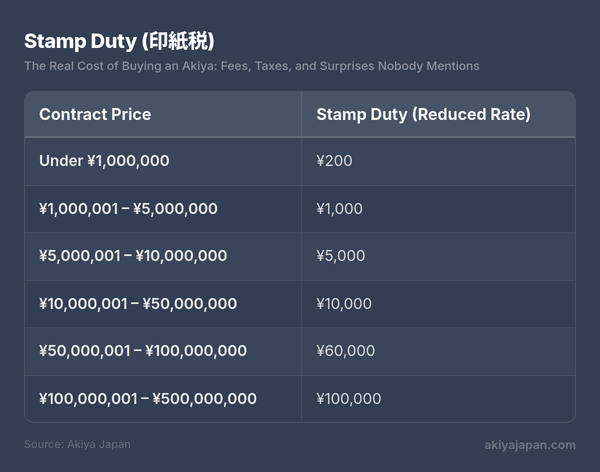

Stamp Duty (印紙税 (inshi-zei))

The purchase contract itself requires revenue stamps (収入印紙) affixed to it. The amount depends on the stated contract price:

The reduced rates shown above have been extended multiple times and apply to contracts for real estate sales. For most akiya purchases, stamp duty is a minor cost — ¥200 to ¥10,000 in the typical range.

Judicial Scrivener Fees (司法書士 (shihō shoshi)報酬)

A judicial scrivener (司法書士 (shihō shoshi) / shihō shoshi) is a licensed professional who handles the legal registration of property transfers. Think of them as a specialized conveyancer. Their role includes:

- Conducting title searches and verifying ownership

- Preparing registration applications

- Filing documents with the Legal Affairs Bureau

- Ensuring the transfer is properly recorded

Their fees are not fixed by law (unlike agent commissions), but typical ranges are:

- Simple ownership transfer: ¥100,000 – ¥150,000

- Transfer with mortgage registration: ¥150,000 – ¥200,000

- Complex cases (multiple parcels, inheritance issues, address corrections): ¥200,000 – ¥300,000

Rural akiya often fall into the "complex" category. The land may be split across multiple parcels (it is not unusual for a single property to sit on 3-5 separate registered lots). The seller's registered address may not match their current address, requiring additional filings. And if the property was inherited, the chain of title may need to be established through multiple generations.

Budget ¥150,000 as a baseline, and up to ¥300,000 if there are any complications.

Real Estate Acquisition Tax (不動産 (fudōsan)取得税 (fudōsan shutoku-zei))

This is the tax that catches people off guard. It arrives 3-6 months after the purchase, by mail, with a payment deadline. By that point, many buyers have already spent their "buffer" budget on initial repairs or furnishing.

The rate is:

- Land: 3% of assessed value (with the assessed value further reduced by half for the calculation)

- Residential buildings: 3% of assessed value

- Non-residential buildings: 4% of assessed value

Again, this is based on the assessed value, not the purchase price. And there are deductions available:

- For buildings used as primary residence meeting certain age and size requirements, deductions of ¥1,200,000 or more from the assessed value before calculation

- For land purchased with a qualifying residential building, significant reductions apply

For a typical akiya with a land assessed value of ¥2,000,000 and building assessed value of ¥500,000:

- Land: (¥2,000,000 × 50%) × 3% = ¥30,000

- Building: ¥500,000 × 3% = ¥15,000

- Total: ¥45,000

On older akiya with low assessed values, this tax is often modest. But on newer or well-located properties where assessed values are higher, it can be a meaningful sum. The critical thing is to set this money aside at the time of purchase so you are not scrambling when the notice arrives.

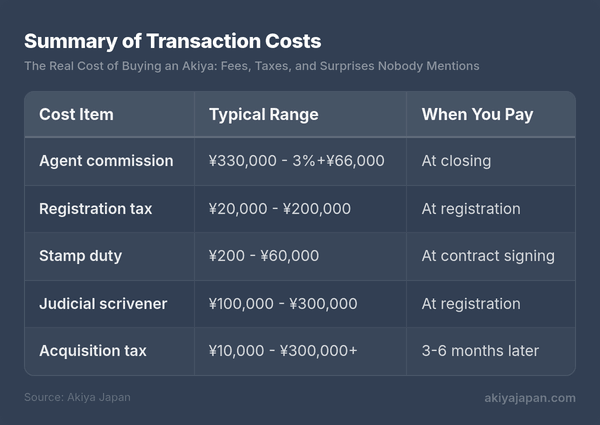

Summary of Transaction Costs

Annual Ongoing Costs

Owning property in Japan means ongoing annual tax obligations, regardless of whether you live in the property, rent it out, or leave it vacant.

Fixed Asset Tax (固定資産税 (kotei shisan-zei)) — 1.4%

Every January 1st, the owner of record is assessed fixed asset tax at 1.4% of the assessed value. This is the universal property tax that applies everywhere in Japan.

There is an important residential land exemption: if a residential structure stands on the land, the taxable assessed value of the land is reduced to 1/6th for lots up to 200 m² (and 1/3rd for the portion exceeding 200 m²). This exemption is one reason people keep dilapidated houses standing rather than demolishing them — tearing down the house can cause the land tax to increase six-fold.

Example: Land assessed at ¥3,000,000 with a house on it:

- With house: (¥3,000,000 ÷ 6) × 1.4% = ¥7,000/year

- Without house: ¥3,000,000 × 1.4% = ¥42,000/year

This six-fold jump is not theoretical — it is the primary reason Japan has so many deteriorating vacant houses that nobody demolishes.

City Planning Tax (都市計画税 (toshi keikaku-zei)) — 0.3%

Properties within urbanization promotion areas (市街化区域) are subject to an additional city planning tax of up to 0.3% of assessed value. Rural properties outside these zones are exempt. If you are buying an akiya in a mountain village or remote coastal town, you likely will not pay this. If you are buying in a suburban area near a regional city, you probably will.

The residential land exemption also applies here, reducing the land portion to 1/3rd (not 1/6th) for lots up to 200 m².

What Annual Taxes Actually Look Like

For a typical rural akiya with land assessed at ¥2,000,000 and building assessed near zero:

- Fixed asset tax: (¥2,000,000 ÷ 6) × 1.4% = approximately ¥4,700

- City planning tax: ¥0 (rural, outside urbanization area)

- Total annual tax: roughly ¥5,000 – ¥15,000

For a suburban property near a regional city with land assessed at ¥8,000,000:

- Fixed asset tax: (¥8,000,000 ÷ 6) × 1.4% = approximately ¥18,700

- City planning tax: (¥8,000,000 ÷ 3) × 0.3% = approximately ¥8,000

- Total annual tax: roughly ¥27,000 – ¥40,000

Annual property taxes in Japan are remarkably low by international standards. For most akiya, you are looking at less than ¥50,000 per year — sometimes far less.

The Hidden Surprises

Here is where budgets unravel. The costs above are predictable and calculable. The costs below are situational — they depend on the specific property — and they are where the real financial risk lies.

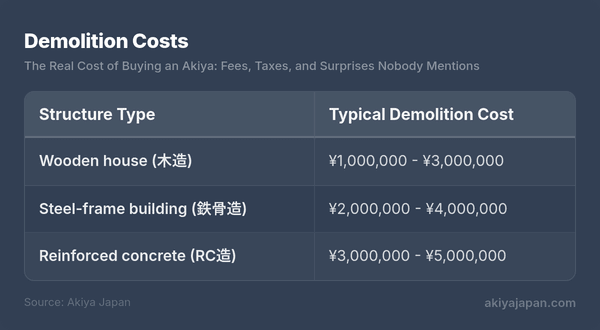

Demolition Costs

If the existing structure is beyond saving, you face demolition costs that can exceed the purchase price several times over:

Costs vary by size, access difficulty (narrow streets increase labor costs significantly), and region. Remote locations may actually be cheaper for the demolition itself but more expensive for waste disposal and transport. And remember the tax implication: demolishing the structure removes the residential land tax exemption, potentially increasing your annual property tax six-fold.

Asbestos Removal

Buildings constructed between the 1950s and 1990s may contain asbestos in insulation, ceiling tiles, siding, or roof materials. Japan did not fully ban asbestos until 2006. If your property contains asbestos and you plan to demolish or significantly renovate, professional removal is required by law.

Costs depend heavily on the extent of contamination, but budget ¥200,000 – ¥1,000,000+ for asbestos survey and removal. A survey alone is ¥30,000 – ¥50,000 and is required before any demolition work. Some municipalities offer subsidies for asbestos surveys and removal — check with the local government before proceeding.

Boundary Surveys (境界確定測量)

In Japan, it is shockingly common for property boundaries to be unclear. Many rural properties have boundaries based on decades-old surveys, verbal agreements with neighbors, or vague references to natural features that have since changed. The boundary stakes (境界杭) may have been removed, buried, or destroyed.

If boundary confirmation is needed (and your agent or scrivener will advise), a licensed surveyor (土地 (tochi)家屋調査士) must be hired. This involves:

- Researching historical records at the Legal Affairs Bureau

- On-site measurement

- Agreement from all adjacent landowners (which can take months if they are deceased, absent, or uncooperative)

- Filing new boundary records

Cost: ¥300,000 – ¥500,000 for a standard residential lot. More for irregularly shaped or large parcels. This cost is often avoidable if the seller already has confirmed boundaries, but for akiya — especially inherited ones — it frequently has not been done.

Water and Sewage Connection

Rural akiya may rely on well water (井戸水) rather than municipal supply. If the well has gone dry, been contaminated, or you want to connect to municipal water:

- Municipal water connection: ¥100,000 – ¥500,000 depending on distance to the nearest main

- Well rehabilitation: ¥200,000 – ¥500,000

- New well drilling: ¥500,000 – ¥1,500,000

For sewage, many rural properties use septic tanks (浄化槽 (jōkasō) / jōkasō) rather than municipal sewer. If the existing septic system is non-functional:

- New septic tank installation: ¥800,000 – ¥1,500,000 (municipal subsidies of up to 50-60% are available in many areas)

- Septic tank maintenance: ¥30,000 – ¥60,000/year for mandatory inspections and pumping

Road Access Issues (接道義務)

Under Japan's Building Standards Act, to rebuild or significantly alter a structure, the property must front a road that is at least 4 meters wide with at least 2 meters of frontage. This is called the setsudō gimu (接道義務) — the road access obligation.

Many old akiya, particularly in historic neighborhoods, do not meet this requirement. The implications are severe:

- You cannot obtain a building permit for new construction

- You can renovate the existing structure but cannot rebuild if it is demolished or destroyed

- The property's value and resale potential are significantly limited

There are workarounds (setback agreements, designated roads, exceptions for special circumstances), but they are complex and not guaranteed. Always verify road access compliance before purchasing — this is one of the most consequential due diligence items for any akiya purchase.

Inherited Property Complications

Many akiya are sold by heirs who inherited the property. Common complications include:

- Unregistered inheritance: The deceased owner is still the registered owner. The heirs must complete inheritance registration before selling, which takes time and requires agreement from all heirs.

- Multiple heirs: Grandparents' property may have been inherited by 4 children, who each have 3 children — meaning 12+ people may need to agree to the sale.

- Outstanding municipal taxes: If the previous owner stopped paying fixed asset tax, the accumulated liability may need to be settled.

- Abandoned personal property: The house may be full of the previous occupant's belongings. Disposal is the buyer's problem unless negotiated otherwise. Budget ¥200,000 – ¥500,000 for professional clearance of a fully furnished house.

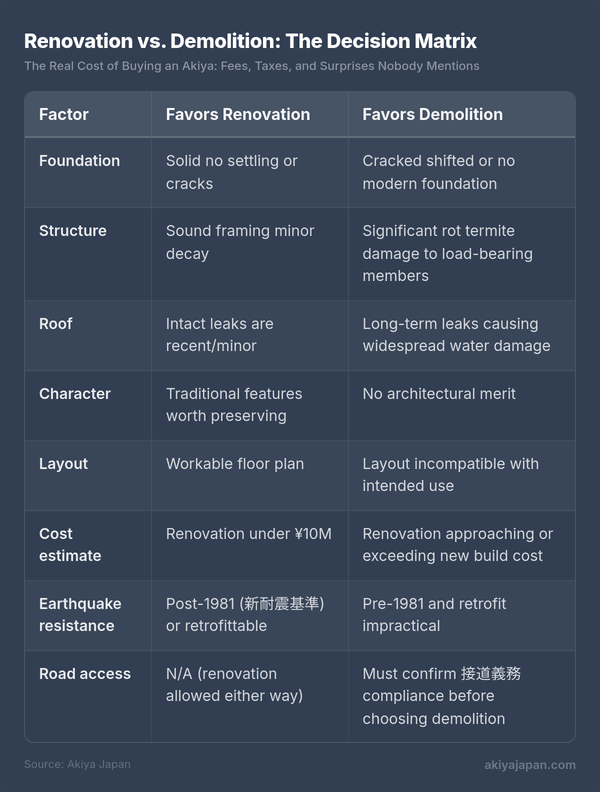

Renovation vs. Demolition: The Decision Matrix

One of the biggest decisions akiya buyers face is whether to renovate the existing structure or demolish and rebuild (assuming road access permits it). Here are the key factors:

The 1981 building code revision is a critical dividing line. Buildings designed under the pre-1981 code (旧耐震 (kyū taishin)基準 (kyū taishin kijun)) lack modern earthquake resistance standards. Bringing them up to code through seismic retrofitting costs ¥1,000,000 – ¥3,000,000, and some structures simply cannot be adequately retrofitted. Many municipalities offer seismic retrofit subsidies of ¥500,000 – ¥1,000,000 — always check before paying out of pocket.

General renovation costs for akiya:

- Cosmetic refresh (paint, flooring, fixtures): ¥1,000,000 – ¥3,000,000

- Moderate renovation (kitchen, bathroom, electrical, plumbing): ¥3,000,000 – ¥8,000,000

- Full renovation (gut and rebuild interior while keeping structure): ¥8,000,000 – ¥15,000,000

- New construction (after demolition): ¥15,000,000 – ¥30,000,000+ depending on size and specification

Insurance

Property insurance in Japan is segmented in ways that can surprise foreign buyers.

Fire Insurance (火災保険)

This is the basic property insurance covering fire, lightning, windstorm, hail, snow damage, water damage from plumbing failures, theft, and vandalism. Despite the name, it covers far more than fire. Premiums depend on:

- Construction type (wooden costs more than RC)

- Location (typhoon-prone areas cost more)

- Building age and condition

- Coverage amount and deductible

Typical annual premiums for a wooden akiya: ¥20,000 – ¥80,000. Policies are now sold in maximum 5-year terms (reduced from 10 years in 2022).

Earthquake Insurance (地震保険)

Earthquake damage is explicitly excluded from fire insurance. Earthquake insurance must be purchased separately and can only be bought as a rider to an existing fire insurance policy — you cannot buy it standalone. Key limitations:

- Coverage is capped at 50% of the fire insurance coverage amount (maximum ¥50,000,000 for buildings)

- Damage is assessed in categories (total loss, large-scale partial, small-scale partial, partial) with fixed payout percentages

- Premiums are set by the government and vary significantly by region and construction type

Annual earthquake insurance premiums: ¥10,000 – ¥50,000 depending on region and structure. Given Japan's seismic activity, this is strongly recommended despite its limitations.

Liability Insurance

If you own a vacant property and someone is injured on it — a child playing in the yard, a delivery person tripping on a broken step, a neighbor's property damaged by your collapsing wall — you are liable. Personal liability insurance (個人賠償責任保険) can be added to your fire insurance policy for a modest additional premium, typically ¥1,000 – ¥3,000/year. This is particularly important for absentee owners who cannot monitor the property's condition.

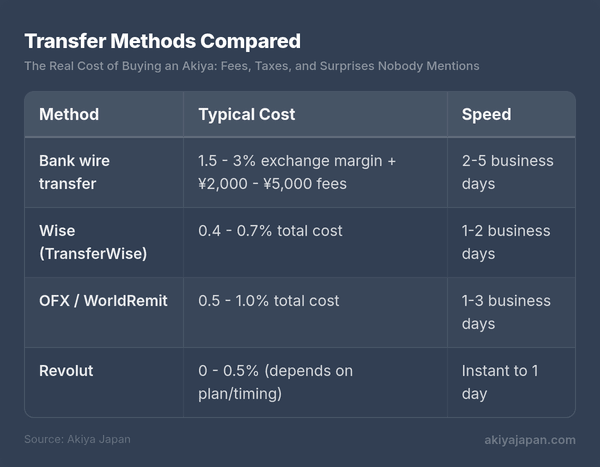

Currency Exchange Costs

If you are buying from outside Japan, converting your home currency to yen is itself a cost center. The spread between buy and sell rates, transfer fees, and timing can materially affect your total outlay.

Transfer Methods Compared

On a ¥5,000,000 transfer, the difference between a bank wire (2% margin) and Wise (0.5%) is approximately ¥75,000 — more than many of the taxes listed above.

Timing Strategies

The JPY/USD and JPY/EUR rates fluctuate significantly. Between 2022 and 2024, the yen weakened dramatically against the dollar, making Japanese property exceptionally cheap for USD buyers. A few practical approaches:

- Dollar-cost averaging: Convert fixed amounts weekly or monthly in the lead-up to your purchase to smooth out rate fluctuations

- Rate alerts: Set target rate alerts on Wise or XE.com and convert when favorable rates hit

- Forward contracts: Some providers (OFX, Moneycorp) offer forward contracts that lock in today's rate for a future transfer, useful if you have a known closing date

Do not try to time the market perfectly. The goal is to avoid converting a large sum at a single unfavorable moment.

Putting It All Together: Three Budget Examples

These examples show realistic all-in costs for three common akiya purchase scenarios. Renovation costs are excluded — these are purely acquisition costs.

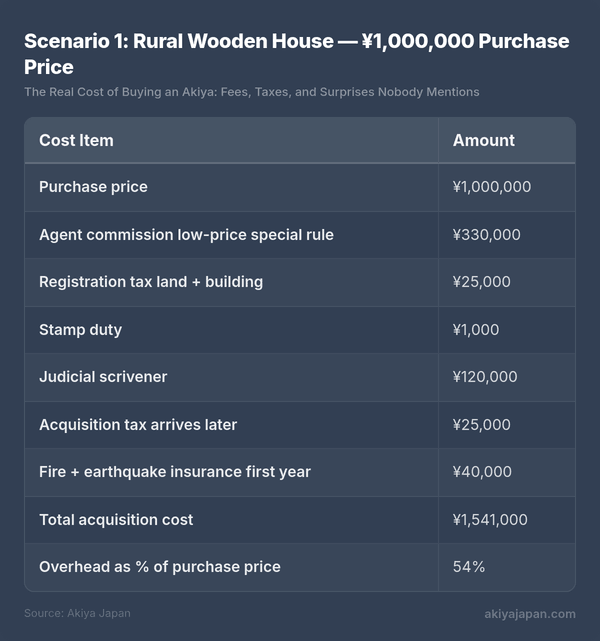

Scenario 1: Rural Wooden House — ¥1,000,000 Purchase Price

A small wooden house in a rural mountain village, 40+ years old, liveable but dated. Simple title, single parcel.

Annual ongoing costs: fixed asset tax ¥5,000 – ¥10,000, insurance ¥30,000 – ¥40,000.

The ¥1,000,000 house actually costs ¥1,541,000 before you spend a single yen on renovation. If you need to clear out the previous owner's belongings (¥200,000+), fix the plumbing (¥300,000+), and do basic cosmetic work (¥1,000,000+), your realistic budget is ¥3,000,000 – ¥4,000,000 all in.

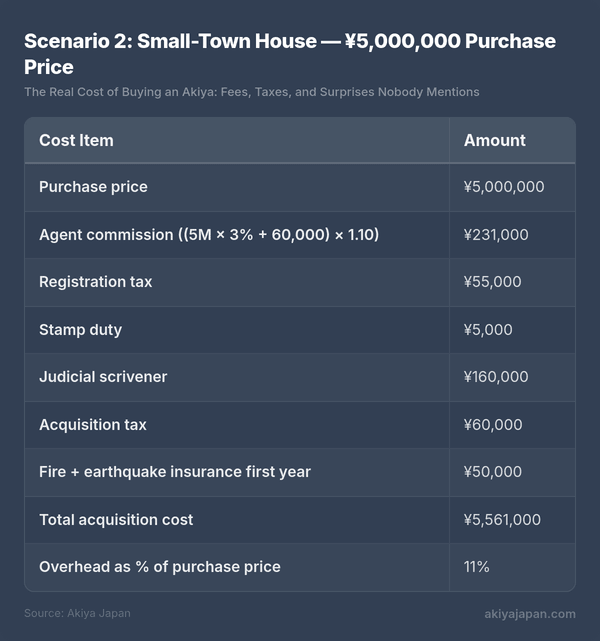

Scenario 2: Small-Town House — ¥5,000,000 Purchase Price

A two-story house in a small city, 25 years old, near a train station. Two parcels of land, clean title, needs moderate updating.

Annual ongoing costs: fixed asset tax ¥15,000 – ¥30,000, city planning tax ¥0 – ¥8,000, insurance ¥40,000 – ¥50,000.

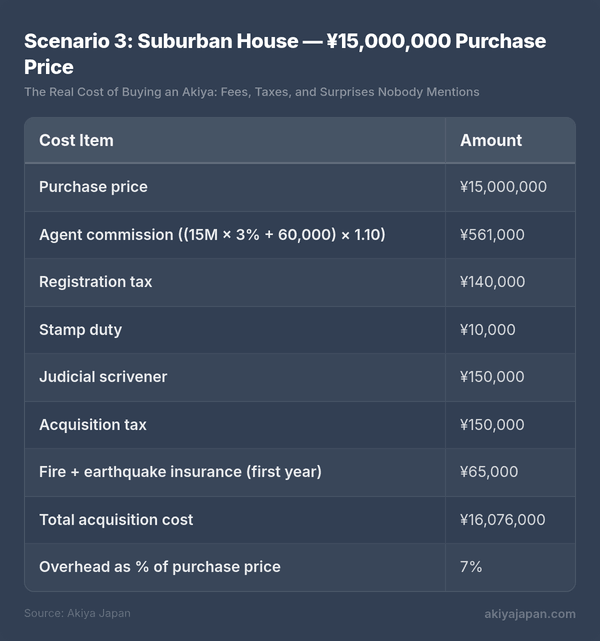

Scenario 3: Suburban House — ¥15,000,000 Purchase Price

A well-maintained house in a suburban area near a regional capital, 15 years old, move-in ready. Proper boundaries confirmed, single large parcel.

Annual ongoing costs: fixed asset tax ¥40,000 – ¥70,000, city planning tax ¥8,000 – ¥15,000, insurance ¥50,000 – ¥65,000.

The Pattern

Notice how the overhead percentage drops sharply as the purchase price rises: 54% on a ¥1M property, 11% on ¥5M, 7% on ¥15M. This is because many costs (scrivener, agent minimum, registration) are semi-fixed or have floors. The ¥1,000,000 akiya dream is real, but your actual budget needs to be at least ¥1,500,000 for acquisition alone.

Costs That Are Often Overlooked

Beyond the main categories above, several smaller costs tend to slip through budget planning:

- Travel costs: At least one trip to Japan for property viewing and closing. International flights, domestic transport, accommodation, and meals during the property search phase can easily reach ¥200,000 – ¥500,000.

- Translation and interpretation: If your agent does not provide bilingual service, independent translation of contracts and documents costs ¥30,000 – ¥100,000.

- Utility connection fees: Reconnecting electricity, gas, and water to a long-vacant property may involve inspection fees or reconnection charges of ¥10,000 – ¥50,000.

- Property management: If you are an absentee owner, a local property management service to check the property monthly, ventilate it, manage mail, and handle emergencies costs ¥5,000 – ¥20,000/month.

- Vegetation management: Overgrown properties must be maintained. Neighbors and municipalities can and do complain (and in some cases, municipalities can order maintenance at the owner's expense). Annual garden maintenance: ¥30,000 – ¥100,000.

- Capital gains tax on sale: If you later sell the property at a profit, capital gains tax applies at 30.63% (short-term, held under 5 years on January 1st of the sale year) or 15.315% (long-term, held 5+ years). Non-residents pay the same rates but withholding rules differ.

Income Tax for Non-Resident Owners

If you rent out your property while living outside Japan, rental income is subject to Japanese income tax. A tax agent (納税管理人 (nōzei kanri-nin)) must be appointed in Japan to handle filings. The tenant (or property manager) is required to withhold 20.42% of gross rent and remit it to the tax office. You then file an annual return to claim deductions (depreciation, repairs, management fees, insurance) and reconcile the withholding.

This is manageable but requires either a Japanese tax accountant (¥50,000 – ¥150,000/year) or sufficient Japanese language and tax knowledge to self-file.

Municipal Subsidies and Grants

The silver lining in all of this: many Japanese municipalities are actively trying to reduce their akiya count and attract new residents, especially to rural areas. Available subsidies vary enormously by location but commonly include:

- Renovation subsidies: ¥500,000 – ¥5,000,000 toward qualifying repair work (most common)

- Seismic retrofit subsidies: ¥500,000 – ¥1,000,000 for earthquake-proofing older homes

- Demolition subsidies: ¥200,000 – ¥1,000,000 for removing dangerous structures

- Moving incentives: Cash grants for relocating to the municipality, sometimes ¥1,000,000+ for families with children

- Septic system subsidies: Up to 50-60% of installation cost in areas without municipal sewer

These subsidies typically require you to live in the property (not use it as a vacation home) and may have residency duration commitments. Availability and terms change frequently — always confirm directly with the local municipal office before factoring subsidies into your budget.

A Realistic Approach to Budgeting

Based on the breakdown above, here is a practical budgeting framework:

- Transaction costs: Add 10-15% to the purchase price (20-50% for properties under ¥3,000,000)

- Contingency for hidden issues: Reserve an additional 10-20% of the purchase price for unexpected costs discovered after purchase

- Renovation (if planned): Get multiple quotes before purchasing and add 20% buffer — renovation in rural Japan frequently costs more than initial estimates due to material transport, specialist availability, and scope creep once walls are opened

- First-year operating costs: Budget ¥100,000 – ¥200,000 for taxes, insurance, utilities, and basic maintenance even if you are not yet living in the property

The most common mistake foreign akiya buyers make is budgeting only for the purchase price and a vague "renovation fund." The transaction costs, delayed taxes, and hidden physical issues can collectively exceed the purchase price on cheap properties. Know the numbers, build in margins, and you will be far better positioned than most buyers entering this market.

Japan's akiya market offers strong value compared to real estate in most developed countries. Annual property taxes that amount to less than a monthly utility bill, no restrictions on foreign ownership, freehold title — these are real advantages. But they only benefit you if you go in with clear-eyed budgeting and an understanding of every cost between "listed price" and "keys in hand."