Japan's property tax system intimidates many foreign buyers at first glance. Six different taxes, Japanese terminology, municipal variations, and rules that change based on property type and location. But here's the truth: for most akiya and affordable property purchases, the actual annual tax burden is remarkably low — often less than ¥10,000 per year. This guide breaks down every tax you'll encounter, with real calculations for properties at price points foreign buyers actually purchase.

The Two Annual Property Taxes

Once you own property in Japan, you'll pay one or two taxes every year. That's it. No wealth tax, no council tax, no complex assessment appeals process. The system is straightforward, and for inexpensive properties, the amounts are remarkably small.

Fixed Asset Tax (固定資産税 (kotei shisan-zei) / Kotei Shisan Zei)

This is Japan's primary property tax, and every property owner pays it. The rate is 1.4% of the assessed value — not the market value or purchase price, but the value determined by the local municipality.

This distinction matters enormously. Assessed values (評価額 (hyōka-gaku) / hyouka-gaku) are typically 50–70% of market value for land and even lower for older buildings. Municipalities reassess properties every three years, and the assessed value of buildings decreases over time as they depreciate. For a 30-year-old wooden house — the kind of structure on most akiya — the building's assessed value may be close to zero.

The Residential Land Exemption

Japan offers a significant tax reduction for land with a residential building on it:

- Small residential land (up to 200㎡): Assessed at 1/6 of the standard value for Fixed Asset Tax purposes

- General residential land (over 200㎡): The portion exceeding 200㎡ is assessed at 1/3 of the standard value

Since most akiya sit on plots under 200㎡, the full 1/6 reduction typically applies to the entire land portion. This is the single most significant tax benefit for property owners in Japan, and it applies automatically as long as a residential structure exists on the land.

City Planning Tax (都市計画税 (toshi keikaku-zei) / Toshi Keikaku Zei)

This secondary tax applies only in urbanization promotion areas (市街化区域 / shigaika kuiki) — zones designated for urban development. The maximum rate is 0.3%, though some municipalities charge less.

Many rural and semi-rural properties, including a large proportion of akiya, fall outside these zones and are completely exempt from City Planning Tax. If your property is in the countryside, a mountain village, or a smaller town, you likely won't pay this at all.

Where it does apply, the residential land exemption also reduces the City Planning Tax base:

- Up to 200㎡: Assessed at 1/3 of standard value (not 1/6 as with Fixed Asset Tax)

- Over 200㎡: Assessed at 2/3 of standard value

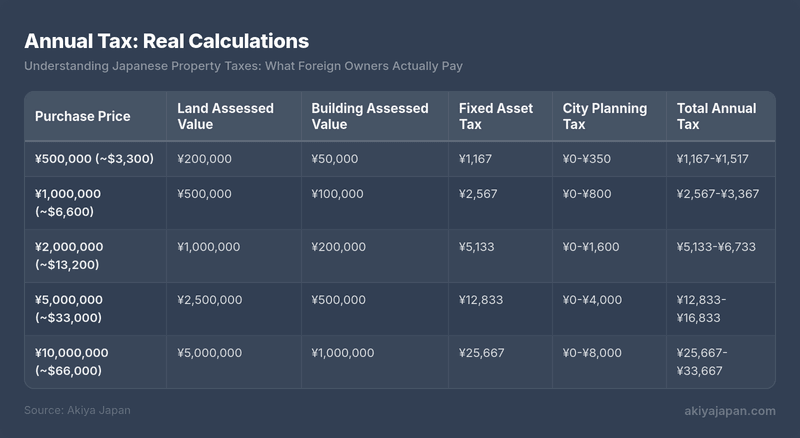

Annual Tax: Real Calculations

The following examples show what owners of typical akiya and affordable properties actually pay each year. These examples assume a property with a residential building (qualifying for the land exemption) on a plot under 200㎡.

Fixed Asset Tax calculation for the ¥1,000,000 example: Land = ¥500,000 × 1/6 × 1.4% = ¥1,167. Building = ¥100,000 × 1.4% = ¥1,400. Total = ¥2,567. City Planning Tax (where applicable): Land = ¥500,000 × 1/3 × 0.3% = ¥500. Building = ¥100,000 × 0.3% = ¥300. Total = ¥800.

Notice the numbers. A ¥2,000,000 property — a common price point for livable akiya — costs roughly ¥5,000–¥7,000 per year in property tax. That's about $35–$45 per year. Many foreign buyers are surprised at how low Japanese property taxes are compared to the US, UK, Canada, or Australia.

Minimum Tax Thresholds

Japan has minimum thresholds below which no tax is levied at all:

- Land: No Fixed Asset Tax if assessed value is below ¥300,000

- Buildings: No Fixed Asset Tax if assessed value is below ¥200,000

Some extremely cheap akiya, particularly those with near-zero building assessments on small plots, may fall below these thresholds entirely, meaning zero annual property tax.

Taxes When You Buy

Beyond the recurring annual taxes, several one-time taxes apply at or shortly after purchase. Understanding these upfront costs prevents surprises.

Real Estate Acquisition Tax (不動産 (fudōsan)取得税 (fudōsan shutoku-zei) / Fudousan Shutoku Zei)

This prefectural tax is levied once when you acquire property, whether by purchase, gift, or construction. The standard rates are:

- Residential land and buildings: 3% of assessed value

- Commercial buildings: 4% of assessed value

The tax is calculated on the assessed value, not the purchase price, so it's significantly lower than it first appears. For residential land, an additional reduction halves the assessment base (assessed value × 1/2), further reducing the burden.

Important timing note: This tax bill arrives 3–6 months after purchase. Many foreign buyers are caught off guard because they've already paid all the costs they expected at closing, then receive an unexpected tax notice months later. Budget for it in advance.

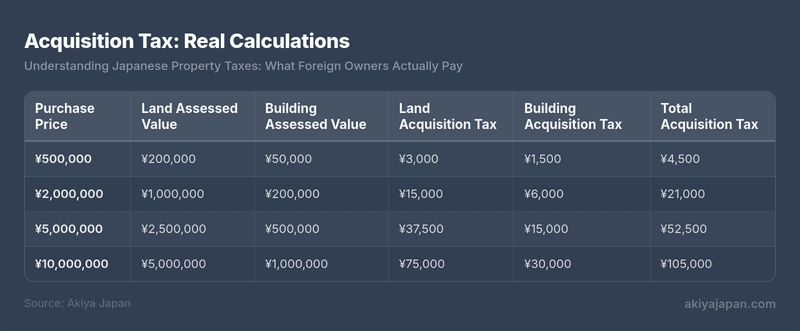

Acquisition Tax: Real Calculations

Land acquisition tax uses the residential reduction: assessed value × 1/2 × 3%. Building acquisition tax: assessed value × 3%. Additional exemptions may apply for newer residential buildings.

Exemptions and Reductions

Several exemptions can reduce or eliminate Real Estate Acquisition Tax:

- Building exemption: Residential buildings assessed below ¥2,300,000 (or built before specific dates with corresponding deduction amounts) may qualify for a deduction from the assessed value before tax is calculated

- Land exemption: If you build or acquire a residential building on the land, additional land tax reductions apply, potentially reducing the land portion to zero for smaller properties

- Newly built homes: A ¥12,000,000 deduction from building assessed value for new construction meeting floor area requirements (50–240㎡)

Exemptions are not always applied automatically. In some cases, you must file an application with the prefectural tax office within a specified period. Your judicial scrivener (司法書士 (shihō shoshi)) or real estate agent should handle this, but confirm it explicitly.

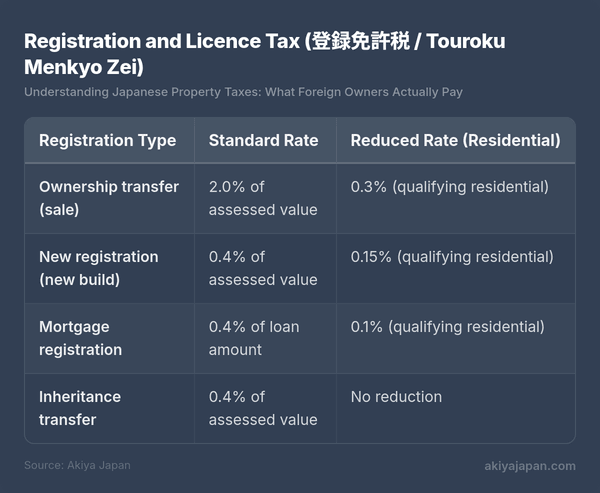

Registration and Licence Tax (登録免許税 (tōroku menkyo-zei) / Touroku Menkyo Zei)

When property ownership is registered at the Legal Affairs Bureau (法務局 (hōmu kyoku)), you pay a national tax based on the type of registration:

The reduced residential rates apply to buildings that meet certain conditions: the buyer must use it as their primary residence, the floor area must be between 50㎡ and 240㎡, and for used homes, additional age or earthquake resistance criteria may apply. Most akiya purchases by foreign owners who won't be residing in Japan full-time will use the standard 2.0% rate for the ownership transfer.

For a property with a total assessed value of ¥1,500,000, the registration tax at the standard rate would be ¥30,000 (~$200). This is typically handled by the judicial scrivener as part of the closing process.

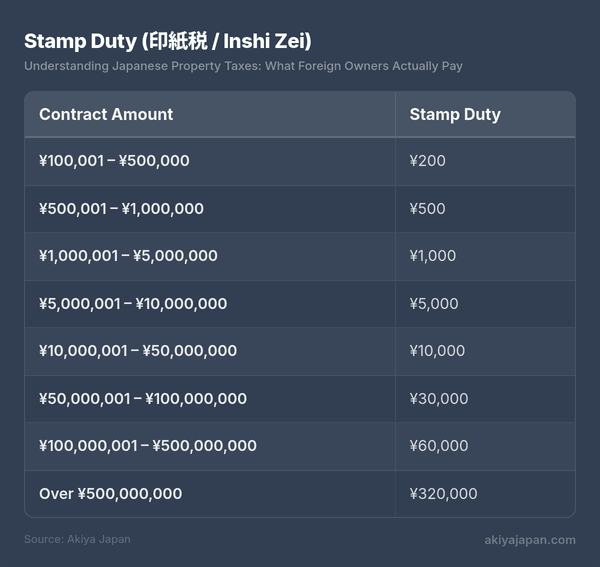

Stamp Duty (印紙税 (inshi-zei) / Inshi Zei)

Revenue stamps must be affixed to the property sale contract. The amount depends on the contract value:

These are the reduced rates under the current tax relief measures. Standard rates are higher but the relief has been consistently extended.

For the vast majority of akiya purchases, stamp duty is between ¥200 and ¥5,000 — essentially negligible.

Consumption Tax (消費税 / Shouhi Zei)

Japan's consumption tax (currently 10%) has specific rules for real estate:

- Land is always exempt — no consumption tax on land, regardless of seller

- Buildings from commercial sellers: 10% consumption tax applies when a real estate company, developer, or business entity sells a building

- Buildings from private sellers: No consumption tax when an individual sells their own property

Since most akiya are sold by private individuals (or their heirs), consumption tax rarely applies to these transactions. When buying from a real estate company that has purchased and renovated a property for resale, expect 10% on the building portion of the price.

Agent commissions and judicial scrivener fees are also subject to 10% consumption tax, but these are service fees rather than property taxes.

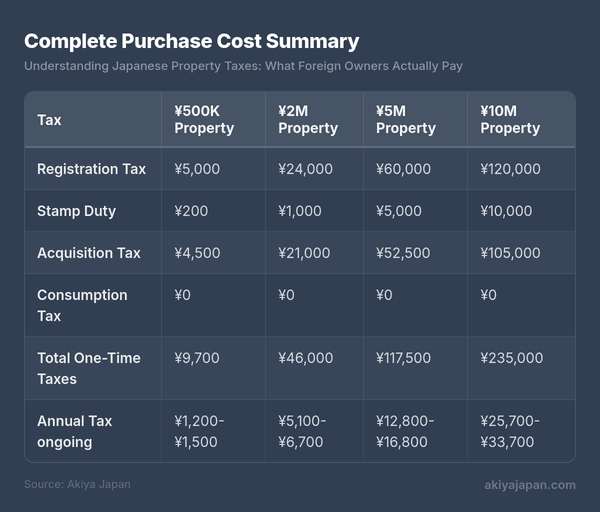

Complete Purchase Cost Summary

Here's a consolidated view of all taxes for typical akiya purchases, assuming a private seller and standard (non-reduced) registration rates:

Consumption tax shown as ¥0 assuming a private seller. Add 10% of the building's sale price if buying from a commercial entity. Acquisition tax arrives 3–6 months after purchase.

Non-Resident Specific Concerns

Foreign owners who don't reside in Japan face additional requirements and tax considerations. None of these are prohibitively difficult, but they require planning.

Tax Representative (納税管理人 (nōzei kanri-nin) / Nouzei Kanrinin)

If you live outside Japan, you must appoint a tax representative — someone residing in Japan who will receive tax notices and handle payments on your behalf. This is a legal requirement, not optional.

Your tax representative can be:

- A friend or acquaintance living in Japan

- Your property management company

- A tax accountant (税理士 / zeirishi)

- Your judicial scrivener or real estate agent (some offer this service)

You designate your tax representative by filing a notification (納税管理人 (nōzei kanri-nin)届出書) with the relevant municipal tax office. Your judicial scrivener typically handles this as part of the purchase process. Professional tax representative services generally cost ¥30,000–¥50,000 per year, though informal arrangements with acquaintances may cost nothing.

Paying Taxes from Abroad

Property tax bills are sent to your tax representative, who can pay on your behalf. Payment methods include:

- Bank transfer from a Japanese bank account (if you have one)

- Convenience store payment using the payment slip (your representative does this in person)

- Credit card payment through certain municipal websites (availability varies)

- Direct debit from a Japanese bank account (set up once, automatic thereafter)

The simplest long-term solution is a Japanese bank account with direct debit. If you don't have a Japanese bank account, your tax representative handles the physical payment process and you reimburse them via international transfer.

Withholding on Rental Income

If you rent out your Japanese property while living abroad, the tenant (or property management company) must withhold 20.42% of gross rental income and remit it to the tax office on your behalf. This withholding applies to non-residents regardless of nationality.

You can file a Japanese tax return to claim deductions (maintenance, depreciation, management fees, insurance) and potentially receive a refund of excess withholding. A tax accountant in Japan can file this return for you, typically for ¥50,000–¥150,000 depending on complexity.

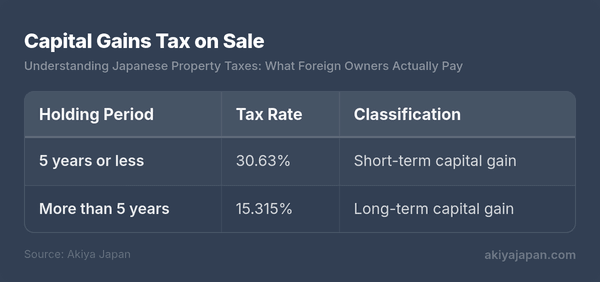

Capital Gains Tax on Sale

When you sell Japanese property, capital gains tax applies based on how long you've owned it:

The holding period is measured from January 1st of the year after acquisition to January 1st of the year of sale. This means a property purchased in December 2024 would need to be held until January 2030 to qualify for the long-term rate — effectively just over five years of actual ownership.

Capital gains are calculated as: sale price minus (acquisition cost + transfer expenses). Acquisition cost includes the purchase price, agent fees, registration costs, and stamp duty. Transfer expenses include agent fees and other costs incurred to make the sale. If you cannot prove the original acquisition cost, 5% of the sale price is used instead — a rule that significantly increases the taxable gain. Keep all purchase documentation.

For non-residents, the buyer is required to withhold 10.21% of the sale price and remit it to the tax office. You then file a tax return to reconcile the withholding against your actual tax liability.

Tax Treaties and Double Taxation

Japan has tax treaties with over 70 countries, including the US, UK, Canada, Australia, France, Germany, and most other major economies. These treaties generally follow a consistent pattern for real estate:

- Property taxes and capital gains on real estate are taxed in the country where the property is located (Japan)

- Your home country grants a credit or exemption for taxes already paid to Japan, preventing you from being taxed twice on the same income or gain

- Rental income is taxable in Japan first, with a credit available in your home country

The practical effect: you pay Japanese taxes on your Japanese property, then claim a foreign tax credit on your home country tax return. In most cases, you won't pay significantly more in total than you would have paid to either country alone.

Consult a tax professional familiar with both Japan's tax system and your home country's treatment of foreign property income. The interaction between two countries' tax codes is where complexity increases considerably.

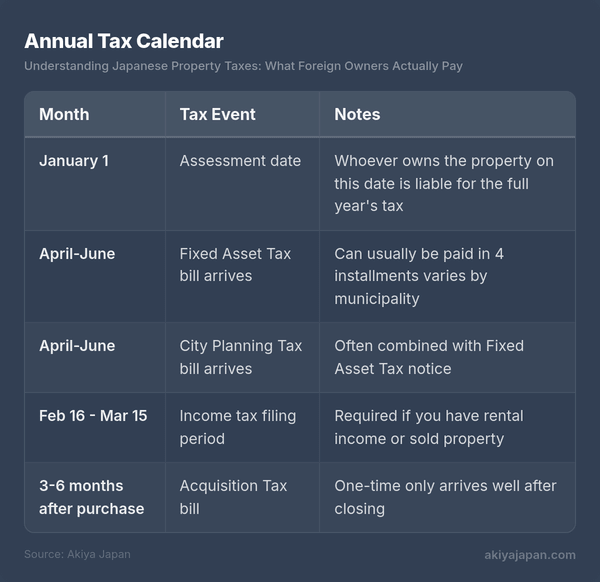

Annual Tax Calendar

Knowing when tax bills arrive helps with budgeting and ensures nothing falls through the cracks:

Fixed Asset Tax can typically be paid in four quarterly installments. The exact payment months vary by municipality but commonly fall in April/May, July, September/October, and December/January. You can also pay the full year at once with the first installment.

Key date: January 1. The person registered as owner on January 1 is responsible for the entire year's property tax. If you buy a property in March, the seller technically owes the full year's tax. In practice, buyer and seller prorate the tax at closing — you reimburse the seller for the portion of the year after your purchase date. This is handled as part of the settlement process, not as a separate tax payment.

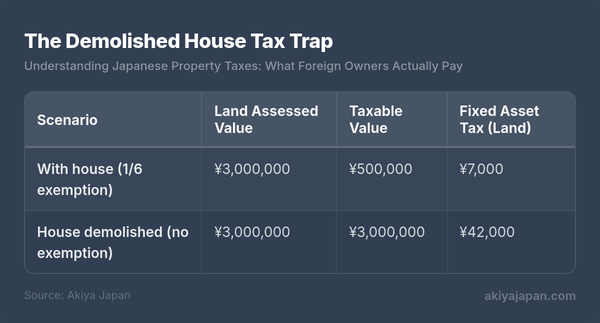

The Demolished House Tax Trap

More foreign owners are blindsided by this than any other tax issue — understand it clearly before you make any decisions about a dilapidated structure on your land.

Remember the residential land exemption that reduces your land's taxable value to 1/6? That exemption requires a residential building to exist on the land. If you demolish the house — even if it's falling apart and uninhabitable — you lose the exemption.

The practical impact:

That's a six-fold increase in land tax. For properties where City Planning Tax also applies, the increase is compounded further (from 1/3 to full value).

This rule is precisely why Japan has so many vacant, deteriorating houses. Owners face a perverse incentive: keeping a crumbling structure standing is significantly cheaper than demolishing it and paying full land tax on an empty lot. It's one of the driving forces behind the akiya phenomenon itself.

When Demolition Still Makes Sense

Despite the tax increase, demolishing may be the right choice if:

- You plan to build a new house immediately — the exemption returns once a new residential structure exists

- The building is designated as a 特定空家 (tokutei akiya / specified vacant house) by the municipality, which can result in losing the exemption anyway

- The absolute tax amount is still small enough that the increase is manageable (on a ¥500,000 assessed plot, the difference is only about ¥5,800 per year)

- You want to use the land for non-residential purposes such as parking or agriculture

Since 2023, municipalities have expanded their authority to designate poorly managed vacant properties as 管理不全空家 (kanri fuzen akiya / inadequately managed vacant houses), which can also trigger loss of the residential land exemption. The message is clear: if you own an akiya, maintain it to at least a minimum standard or face higher taxes regardless.

Putting It All Together: Total Cost of Ownership

The complete five-year tax picture for three realistic purchase scenarios:

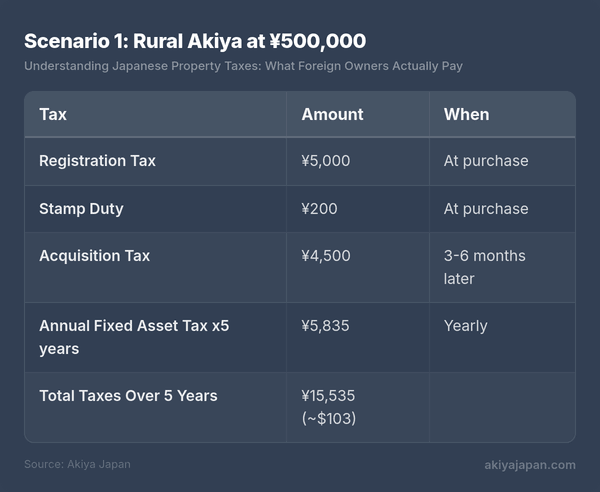

Scenario 1: Rural Akiya at ¥500,000

A countryside house on a small plot, no City Planning Tax zone.

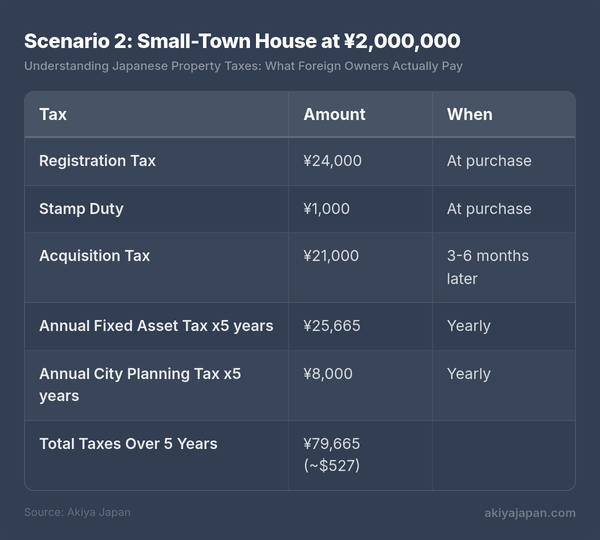

Scenario 2: Small-Town House at ¥2,000,000

A house in a small city, within the City Planning Tax zone.

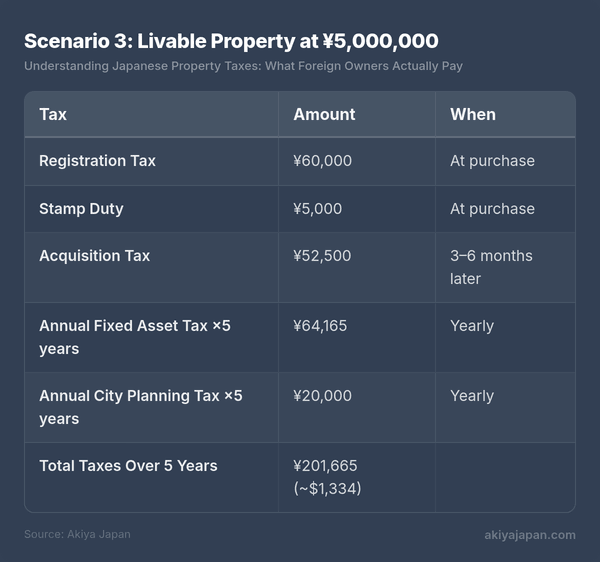

Scenario 3: Livable Property at ¥5,000,000

A well-maintained house in a regional city, City Planning Tax applies.

Even at the ¥5,000,000 level, total taxes over five years amount to roughly $1,300. Compare that to a similarly priced property in most Western countries and the difference is stark. Japanese property taxes are, by international standards, very low.

Common Questions

Do foreigners pay higher property taxes?

No. Japan's property tax system makes no distinction based on nationality or residency status. A foreign owner and a Japanese owner of identical properties pay exactly the same Fixed Asset Tax and City Planning Tax. The only differences for non-residents are procedural: appointing a tax representative and the withholding rules on rental income and capital gains.

What happens if I don't pay property tax?

Unpaid property taxes accrue a delinquency charge (延滞金 / entaikin) at roughly 8–9% per year. After extended non-payment, the municipality can place a lien on the property and ultimately seize it through auction. In practice, for the small amounts involved with cheap akiya, municipalities are often willing to work out payment arrangements. But ignoring tax bills is never advisable — it creates complications if you later want to sell or transfer the property.

Can I deduct Japanese property taxes on my home country taxes?

In most cases, yes. Property taxes paid to Japan are typically deductible or creditable on your home country tax return, depending on the specific provisions of your country's tax code and any applicable tax treaty. US taxpayers, for example, can claim foreign tax credits for Japanese taxes on their federal return. Consult your home country tax advisor for specifics.

How do I find out my property's assessed value?

The assessed value appears on your annual Fixed Asset Tax notice (固定資産税 (kotei shisan-zei)納税通知書). You can also request a valuation certificate (評価証明書 / hyouka shoumeisho) from the municipal tax office. During the spring review period (typically April), property owners can inspect the tax rolls (縦覧 / juran) to compare their assessed values with similar properties in the area.

Is there a property tax for vacant land I buy without a building?

Yes, but without a residential building, the land doesn't qualify for the 1/6 exemption. You'll pay Fixed Asset Tax at the full 1.4% of assessed value (and City Planning Tax at 0.3% if applicable). This is why vacant land sometimes has higher annual taxes than land with a house on it, despite being worth less overall.

Key Takeaways

- Annual property taxes are based on assessed value, which is significantly lower than market or purchase price

- The residential land exemption (1/6 reduction) dramatically lowers land tax for properties with a house — don't demolish without understanding the consequences

- One-time purchase taxes (registration, stamp duty, acquisition tax) are modest and based on assessed values

- Acquisition tax arrives months after purchase — budget for it in advance

- Non-residents must appoint a tax representative in Japan to receive and pay tax bills

- Capital gains tax drops by half if you hold the property more than 5 years (30.63% to 20.315%)

- Tax treaties prevent double taxation in most cases — but get professional advice for your specific situation

- For cheap akiya, total taxes over five years can be under ¥20,000 (~$130) — property tax is rarely a meaningful factor in the ownership decision

For buyers comparing acquisition costs across regions, browse houses for sale in Japan — updated daily — or see cheap houses under ¥5,000,000, where annual property tax typically stays under ¥10,000.