If you're a foreigner hoping to finance an akiya purchase with a Japanese mortgage, you almost certainly can't. But that doesn't mean buying is out of reach — it just means you need a different approach.

The Japanese banking system wasn't built with foreign akiya buyers in mind. Between strict residency requirements, minimum loan thresholds, and the way Japanese banks value aging wooden buildings, the financing situation can feel like a wall of "no." This guide explains exactly why banks reject most akiya financing applications, which institutions might say yes under the right circumstances, and — most importantly — the alternative strategies that actually work for foreign buyers.

Why Japanese Banks Say No

It's not personal. Japanese mortgage lending follows a set of structural rules that make akiya financing impractical from the bank's perspective, regardless of your financial standing back home.

The building has zero book value

This is the single biggest obstacle, and most foreign buyers don't see it coming. Japanese banks assess property value using a statutory useful life system. For wooden residential buildings — which account for the vast majority of akiya — that useful life is 22 years. Once a wooden house passes its 22nd birthday, its assessed building value drops to zero, regardless of its actual condition.

Think about what this means: a beautifully maintained 30-year-old farmhouse with new roofing and modern plumbing is worth exactly the same as a collapsing ruin on paper. The bank sees both as land value only. And in rural Japan, land value alone is often too low to justify a mortgage.

This isn't a quirk — it's fundamental to how Japanese real estate works. Unlike most Western countries, where older homes can appreciate in value, Japan's tax and banking systems treat buildings as depreciating assets, much like cars. A house loses roughly 4.5% of its value every year until it hits zero at year 22.

The loan amount is too small to process

Most Japanese banks set minimum mortgage amounts between ¥5 million and ¥10 million (approximately $33,000–$67,000 USD). Many akiya sell for ¥1–5 million, and some are listed for under ¥1 million. The administrative cost of processing, appraising, and servicing a mortgage on a ¥2 million property simply isn't worth it for the bank. They'd spend more on paperwork than they'd earn in interest over the life of the loan.

No Japanese credit history

Japan's credit system is entirely separate from those in other countries. Your 800 FICO score, your spotless payment history with your home bank, your substantial investment portfolio — none of it exists in Japan's credit information system. As far as Japanese banks are concerned, you have no financial track record at all.

Japan uses three credit information agencies — CIC, JICC, and KSC — and they only track financial activity within Japan. Building a credit history requires having Japanese financial products: a Japanese credit card, a Japanese phone contract, Japanese utility bills paid from a Japanese bank account. This takes years, not months.

Residency requirements are strict

Most Japanese banks require one or more of the following to even consider a mortgage application:

- Permanent residency (PR) — the gold standard for mortgage eligibility. Typically requires 10+ years of continuous residence in Japan.

- Spouse visa — married to a Japanese national with stable household income in Japan.

- Long-term resident status — at least 3 years on a qualifying visa with stable employment at a Japanese company.

- Japanese income — documented, taxable income earned in Japan, typically for a minimum of 2–3 consecutive years.

If you live outside Japan and want to buy a vacation property or future retirement home, conventional Japanese mortgages are essentially off the table. Banks want borrowers who are physically present, earning yen, and integrated into the Japanese financial system.

Low collateral value in rural areas

Banks lend against collateral. A ¥50 million apartment in central Tokyo is easy to sell if the borrower defaults — there's always a buyer. A ¥3 million wooden house in a village with a declining population of 2,000? The bank could be stuck with it for years. Rural properties carry high collateral risk, and banks price that risk by simply not lending.

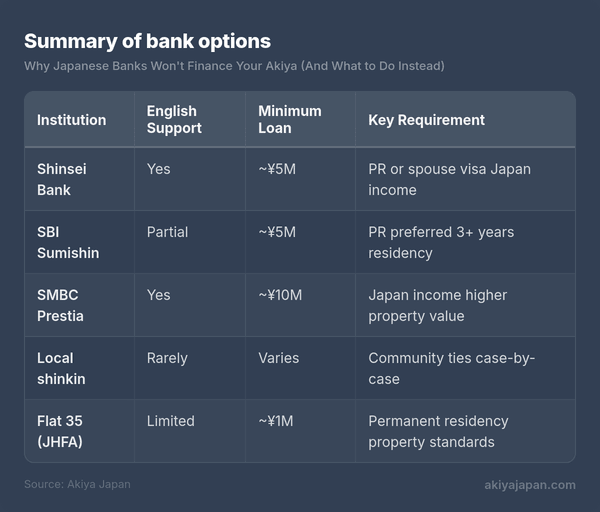

Banks That Do Lend to Foreigners

A small number of Japanese financial institutions will consider mortgage applications from foreign nationals, but every one of them comes with significant conditions. Don't read this section as "these banks will give you a mortgage" — read it as "these are the only doors worth knocking on if you happen to meet the requirements."

Shinsei Bank and SBI Sumishin Net Bank

These are often cited as the most foreigner-accessible options. Both offer some English-language documentation and support staff who can communicate in English. However, both generally require permanent residency or a spouse visa, stable employment in Japan, and the property to meet certain value thresholds. SBI Sumishin has offered mortgages to long-term residents without PR in some cases, but this is evaluated on a case-by-case basis, not a published policy.

SMBC Prestia (formerly Citibank Japan)

SMBC Prestia caters to international clients and provides English-language banking services. They offer mortgage products, but minimum loan amounts typically start at ¥10 million or higher, which immediately excludes most akiya purchases. You'll also need documented income in Japan. Prestia is more realistic for urban apartment purchases than rural akiya.

Local shinkin banks and credit unions

The conventional advice breaks down. Shinkin banks (credit cooperatives) operate at the local level and sometimes have more flexibility than major national banks. In areas where municipalities are actively trying to attract new residents to combat depopulation, local shinkin banks may be more willing to work with unconventional applicants — including foreign nationals with ties to the community.

The catch is that there's no standardized policy. You need to walk into the branch, explain your situation, and hope for a sympathetic loan officer who's willing to escalate your application. Having a Japanese spouse, business partner, or local guarantor dramatically improves your chances. Speaking Japanese — or bringing someone who does — is practically mandatory.

Japan Housing Finance Agency (Flat 35)

The Flat 35 program is a government-backed fixed-rate mortgage available through participating financial institutions. The interest rate is fixed for up to 35 years, which is attractive in any market. Foreign nationals with permanent residency are eligible. The property must meet specific technical standards, which many older akiya won't pass without renovation. Minimum loan amounts and property requirements still apply.

Summary of bank options

Note: Policies change regularly. Minimum amounts and residency requirements listed here are general guidelines — always confirm directly with the institution.

The Renovation Financing Problem

Even if you somehow secure financing for the purchase itself, you'll hit the same wall again when it comes to renovation. And renovation is where the real money goes.

A typical akiya might cost ¥1–5 million to buy, but bringing it up to comfortable, modern living standards can easily cost ¥5–15 million or more. Structural repairs, roof replacement, plumbing and electrical upgrades, insulation, seismic reinforcement — these aren't cosmetic touches. They're essential work on buildings that have often sat vacant for years.

Japanese banks that offer renovation loans (reform loans) face the same collateral problem: they're being asked to lend money to improve a building they consider worthless. Some banks offer combined purchase-and-renovation loans, but these are typically limited to properties that already meet minimum value thresholds — which, again, excludes most cheap akiya.

Renovation loans, when available, tend to have shorter terms (10–15 years), higher interest rates, and lower maximum amounts than standard mortgages. They may also require detailed renovation plans from a licensed contractor before approval.

Alternative Financing Strategies

Here's the good news: the vast majority of foreign akiya buyers don't use Japanese bank financing at all. The property prices are low enough that other strategies work better. Here's what people actually do.

Cash purchase

This is by far the most common approach, and it's worth reframing how you think about it. When a property costs ¥2–5 million ($13,000–$33,000 USD), you're not buying a house the way you would in London or Sydney. You're making a purchase closer in scale to a used car. Many buyers save specifically for an akiya purchase, treating it as a medium-term savings goal rather than a major debt event.

The advantages of cash are significant in Japan:

- Faster closing — cash transactions can close in 4–8 weeks versus 2–3 months with financing.

- Stronger negotiating position — sellers and agents prefer cash buyers, and you may be able to negotiate a lower price.

- No residency requirements — anyone can buy property in Japan for cash, regardless of visa status.

- No ongoing yen-denominated debt — you avoid currency risk on repayments.

- Simpler paperwork — no bank appraisals, no mortgage registration fees, no loan guarantee fees.

Home country equity or HELOC

If you own property in your home country, borrowing against your existing equity can be one of the smartest ways to fund a Japan purchase. A home equity line of credit (HELOC) or home equity loan uses your domestic property as collateral — which your home bank actually knows how to value — and gives you cash to deploy in Japan.

This approach lets you borrow at your home country's rates (often lower than Japanese renovation loan rates for foreigners), using an asset your bank understands, while keeping the Japan transaction simple and cash-based. The main risk is currency exposure: you're borrowing in your home currency but buying an asset denominated in yen.

Municipal subsidies and grants

Most buyers overlook this entirely. Hundreds of Japanese municipalities offer direct financial subsidies for people who purchase and renovate akiya, particularly in depopulating areas. These aren't loans — they're grants that don't need to be repaid.

Typical programs offer:

- Renovation grants of ¥1–5 million for structural improvements to akiya.

- Moving subsidies of ¥100,000–¥300,000 for relocating to the municipality.

- Child-rearing bonuses — additional subsidies per child for families with young children.

- Property tax exemptions for 3–5 years after purchase.

- Reduced or free akiya bank listings — some municipalities list properties for ¥0 if the buyer commits to living there.

The conditions vary widely. Some programs require you to become a resident of the municipality. Some require the renovation to be done by local contractors. Some are limited to applicants under a certain age or to families. And some are explicitly open to foreign nationals — though the application process typically requires Japanese language ability or local assistance.

Municipal subsidies won't cover the full cost of purchase and renovation, but ¥2–3 million in grant funding can make a substantial difference when the property itself costs ¥1–5 million.

Seller financing

Rare, but not impossible. In some cases — particularly with properties listed through municipal akiya banks — the seller may agree to an installment payment plan. This is most likely when the seller is a municipality or estate executor who wants to move the property and is less concerned about receiving full payment immediately.

Seller financing in Japan has no standardized framework, so terms are negotiated directly. You'd want a shiho shoshi (judicial scrivener) to draft a proper agreement and handle the title transfer. Don't expect this to be offered — but if you're dealing with a motivated seller and have local representation, it's worth asking.

Personal loans in your home country

An unsecured personal loan from your home bank won't offer the rates or terms of a mortgage, but for an akiya-scale purchase, the numbers can still work. A $25,000 personal loan at 7–10% over 5 years might cost you $500–600/month in repayments. That's a high cost of capital, but it gets you into a property without waiting years to save the full amount.

Compare the total interest cost against the alternative: waiting 2–3 years to save while property prices, renovation costs, and exchange rates all shift. Sometimes paying a premium for speed makes financial sense.

Combination approach

The most practical strategy for many buyers is a combination:

- Cash for the property purchase (the cheaper part).

- Municipal grants for renovation (apply early — some have annual deadlines).

- Home equity or personal loan for the remaining renovation costs (borrowed in your home currency, against assets your bank understands).

This keeps the Japan side of the transaction clean and cash-based while leveraging your financial standing at home for the more expensive renovation work.

Currency Considerations

If you're funding a purchase from outside Japan, currency exchange becomes a meaningful part of your financial planning. The yen has experienced significant fluctuations, and the rate at which you convert your home currency into yen directly affects your total cost.

Borrowing in yen vs. your home currency

If you borrow in yen (through a Japanese bank), your repayments are in yen. If your income is in another currency, a strengthening yen makes your repayments more expensive. If you borrow in your home currency (HELOC, personal loan), your repayments are predictable, but the value of your yen-denominated asset fluctuates relative to your debt.

Neither approach eliminates currency risk entirely. The key question is: where is your income? If you earn yen, borrow in yen. If you earn dollars, euros, or pounds, borrowing in your home currency and converting to yen for the purchase is generally simpler and more predictable.

Transfer services

Don't use your regular bank for large international transfers — the exchange rate markup and fees can cost you 2–4% of the total amount. Services like Wise (formerly TransferWise), OFX, or Revolut offer significantly better exchange rates and lower fees for large transfers. On a ¥10 million transfer, the difference between a bank and a specialist transfer service can be ¥200,000–¥400,000.

If You Do Qualify: Approaching a Japanese Bank

If you have permanent residency, stable Japanese income, and are looking at a property valued above ¥10 million, a Japanese mortgage becomes a realistic option. Here's how to approach it.

Step 1: Get pre-qualified before you property hunt

Contact the bank before you find a property. Explain your situation — visa status, employment, income, the type of property you're looking for. The bank will tell you quickly whether you're a viable applicant. This saves you the heartbreak of finding a perfect property and then discovering you can't finance it.

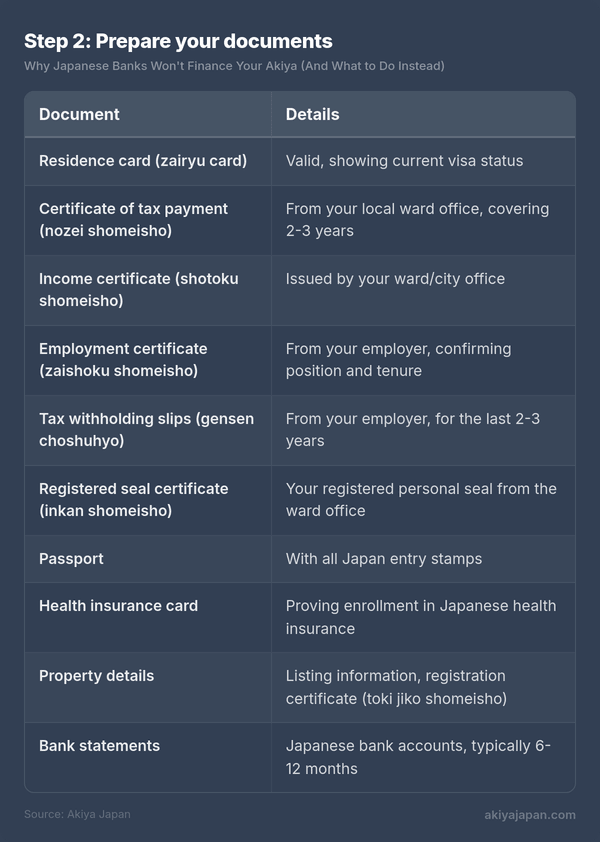

Step 2: Prepare your documents

Japanese mortgage applications require extensive documentation. Having everything ready before you apply shows the bank you're serious and speeds up the process considerably.

If you're self-employed, you'll also need your final tax returns (kakutei shinkoku) for the past 3 years and financial statements for your business.

Step 3: Understand the costs beyond the mortgage

Even with financing approved, you'll need cash for closing costs that can't be rolled into the mortgage:

- Real estate agent commission — up to 3% + ¥60,000 + tax (capped by law).

- Registration and license tax — approximately 1–2% of the assessed property value.

- Stamp duty — ¥10,000–¥60,000 depending on loan amount.

- Mortgage registration tax — 0.4% of the loan amount (reduced to 0.1% for certain primary residences).

- Loan guarantee fee — typically 2% of the loan amount upfront, or a 0.2% interest rate addition.

- Fire insurance — required by the bank, typically ¥100,000–¥300,000 for a multi-year policy.

- Judicial scrivener fees — ¥100,000–¥200,000 for handling registration.

Budget an additional 6–10% of the purchase price for these closing costs. On a ¥10 million property, that's ¥600,000–¥1,000,000 in cash you'll need regardless of your mortgage.

Step 4: Use a bilingual real estate agent

Your agent will be your primary interface with the bank. They've done this before, they know which loan officers to talk to, and they can present your application in the most favorable light. A good bilingual agent is worth their commission several times over when it comes to mortgage applications.

What Actually Works: The Practical Approach

After all the detail above, here's the honest summary of how most foreign akiya purchases actually happen:

The property is bought with cash. The buyer saves up, borrows against home-country assets, or combines both. The Japan side of the transaction involves no lending institution at all. A judicial scrivener handles the title transfer, the buyer pays cash, and the deal closes in weeks rather than months.

Renovation is funded separately. Municipal grants cover a portion. The rest comes from savings, home-country borrowing, or phased renovation spread over months or years. Many buyers do an initial round of essential repairs (roof, plumbing, electrical) and then tackle cosmetic and comfort upgrades gradually as budget allows.

Bank financing is a bonus, not a plan. If your circumstances happen to align — permanent residency, Japanese income, a property above the minimum loan threshold — then explore it. But don't build your akiya purchase strategy around getting a Japanese mortgage. Build it around not needing one.

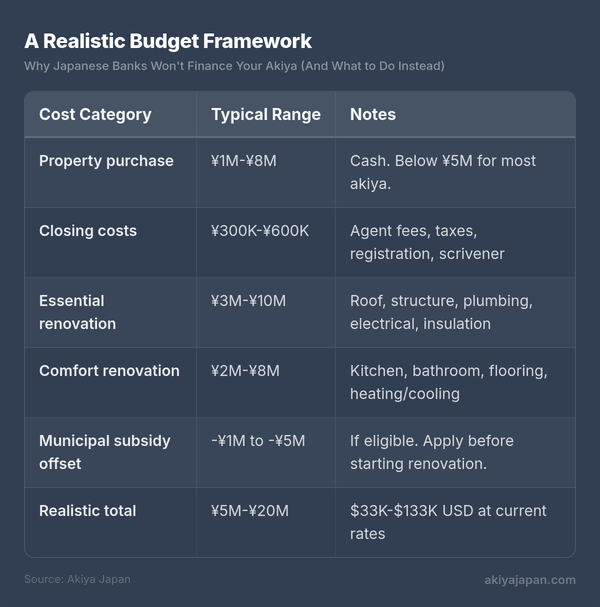

A Realistic Budget Framework

To bring this all together, here's what a typical akiya purchase and renovation budget looks like for a foreign buyer:

That's a wide range, and where you land depends on the property's condition, location, and how much work you want done. But even at the high end, it's a fraction of what a comparable project would cost in most Western countries.

Key Takeaways

- Japanese banks won't finance most akiya purchases by foreigners. The combination of building depreciation rules, residency requirements, minimum loan amounts, and low rural collateral values makes it structurally impractical.

- A few banks will consider applications from PR holders with Japanese income, but only for properties above ¥5–10 million — which excludes the cheapest akiya.

- Cash is king. Most foreign akiya buyers pay cash for the property and fund renovation through savings, home-country borrowing, or municipal grants.

- Municipal subsidies are real money. Research what's available in your target area before you buy. Grants of ¥1–5 million for renovation are not uncommon.

- The property is the cheap part. Budget your renovation costs carefully — they'll typically exceed the purchase price by a factor of 2–5x.

- Don't let financing anxiety stop you. The reason akiya are accessible to foreign buyers is precisely because they're cheap enough to buy without a mortgage.

The Japanese banking system wasn't designed for your akiya purchase. But the akiya market, with its remarkably low entry prices, wasn't designed to need the banking system either. Work with that reality, not against it, and you'll find the path to ownership is simpler than the financing situation makes it appear.